Three important Canadian data points over the past few days:

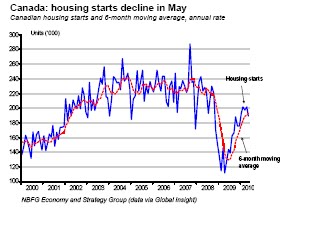

Canadian housing starts were down 6.3% well below consensus expectations. However, we have to keep in mind that the rebound in housing starts observed since April 2009 has been strong. This month’s numbers could be the first signs of the end of a frontloading of the purchasing process by Canadian home buyers. Another important development is related to the multiple segment where there appears to exist excess stock. Residential construction has been a determinant component of the Canadian GDP growth. Initial data therefore (only 2 months of the Q2 period) seem to confirm that housing will not be a net contributor. Although housing only accounts for 6% of Canada

The trade picture is not very rose, although Canada produced a trade surplus +200 million in April (-200 MM in March) the news was not all good, insofar as that the reason for the surplus was a greater drop in import than in exports – (both in price and volume) which speaks weakness of the Canadian economy.

More “poor” economic news on the Canadian auto segment which has seen a (widely anticipated) drop in sales in April (-4.7%). This is the second month of weak sales, and StatsCan has indicated that preliminary numbers for May are flat. Automobile sale are considered a minor data point, but added to the other economic news the 6.1% print for GDP growth in the first quarter is unlikely to repeat.

The trends are troubling and is adds to the growing list of weak Q2 data — trade, housing starts and resale starts. We are tracking 3.3% QoQ at an annual rate GDP growth, below consensus estimates of 3.6% (the Bank’s at 3.8%) and we continue to think that the risks are to the downside.

Finally, and just as a form of “chart porn”, the U.S. US economy, but the V shape is starting to not look like a U shape recovery but like a “hockey stick”, where the US

One think for sure that the hockey Stick theory fits a deleveraging economy!

Comments