Over the past few days new records have been set; Spain saw rates on its new 5y debt at 2.5%, the lowest ever -- and that's a country that has had a debt market for 500 years! Italy saw its debt rate fall to a new low, the same day that the Italian government admitted that it owed more than $100 billion in late payments to its creditors (local suppliers). What's going on, for a start there are no risks in Europe, the ECB has decided that it will buy all paper not absorbed by the market, making peripheral (higher yield) Europe a sure thing for institutional investors, this is particularly true for the short dated instrument (interests could still go up -- and destroy bond values). But deflation is a greater risk (especially since European countries are locked-in with a single currency) its almost an objective of current policies.

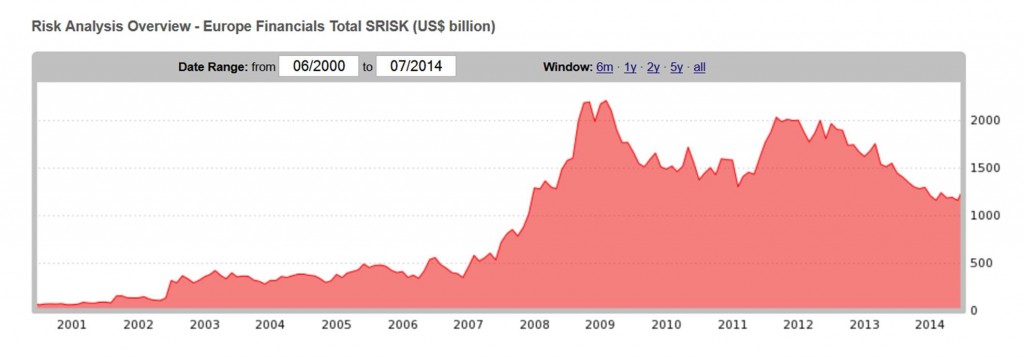

The above graph is very positive for Europe (not good, but positive) insofar as the total debt volume is down, mainly because core Europe has squeezed the public expenditures (hence the massive unemployment), so the picture is still positive,if you compare to 2008 its great, but rather bad compared to 2007! Anyway there we are, Europe's basket cases are borrowing cheaply (in the short end of the curve), there is no fear of inflation in Europe (deflation is the real risk here -- same as in America where the economies are working substantially below potential). So rolling the short dated debt presents limited risk for investors.

It makes perfect sense when you consider that European investors have few "choice" options available. The market is seen as "very bubbly" and most investors are already very long the market -- usually with solid profits buffer in their positions, and are therefore unwilling to buy more with the risk of increasing their average costs. Especially hard to justify investing in the CAC or DAX in view of the rather high multiples (the same is true for the American markets). Sure a P/E of 14 can be justified but its considered high when corporate profits as a percentage of GDP are standing at historical high (its hard to see how they can go higher... although).

So for institutional investors the bond market in Europe is the one place they can go, and the search for yield pushes them to the outer edge of Europe (where by the way the population has already been wiped into submission). Things in France are just starting and the population isn't going to take it lying down, no sir!

Investors are logical give a set of options they will seek maybe not the best solution, but the least bad one at least.

On a side note, a European friend recently told me that it was disgraceful how North America's pension funds were changing the rules on pension holders (I didn't mention that the move to replace defined pension to defined contribution occurred years ago). But I did point out that at least in North America we had pension assets -- while in Europe they have nothing! Just a promise to pay -- maybe. He actually didn't believe me! (ok not really a friend more of an aircraft acquaintance really) I explained to him that in North America the pension assets belong to the "pensioners" while the promise from European governments (and companies) was just that. In fact, I pointed out that after Enron it became illegal for pension funds to invest in their own company (no more than 5% of assets) to avoid having a bankruptcy killing both your job and your pension. I suggested that he check with his own company...

Finally, China does weird stuff -- this video, says so much about China's risk management culture. The video (from a dashcam) shows the demolition of a building in the middle of a city, people are walking nearby unaware that the building is about to go down. Rather spectacular. It reminds me of a book a read a few years ago: Poorly made in China where a shampoo made in China had on the label: "Not tested on animals" which was absolutely true, since that product had not been tested at all!

Recently, GDP growth in China has been lagging from target numbers -- the solution has been to turn the spigots of money creation full on. The imbalance that the Chinese themselves worry about: Investment Vs, Consumption is worse today than it was 4 years ago. Chinese are used to the way things are and are not ready to assume the very real burden that shifting to a consumption society implies.

hence this:

This is very bad

The NYU measure of systemic financial risk for China this year reached an all-time high. This seems to be a result of the fact that liabilities of the Chinese banks have continued to grow rapidly while stock valuations of the institutions appear quite vulnerable to a downturn. The real issue is one of contagion. When Lehman was "let go" no one thought the repercussions would be so dramatic -- really everyone though there would be some limited contagion, turns out the way our world is connected it doesn't work that way. So imagine a Chinese bank walking away from its derivatives obligation to JP Morgan (or DB for that matter) the largest derivates players? I don't know, my bet is that no else has any idea either!

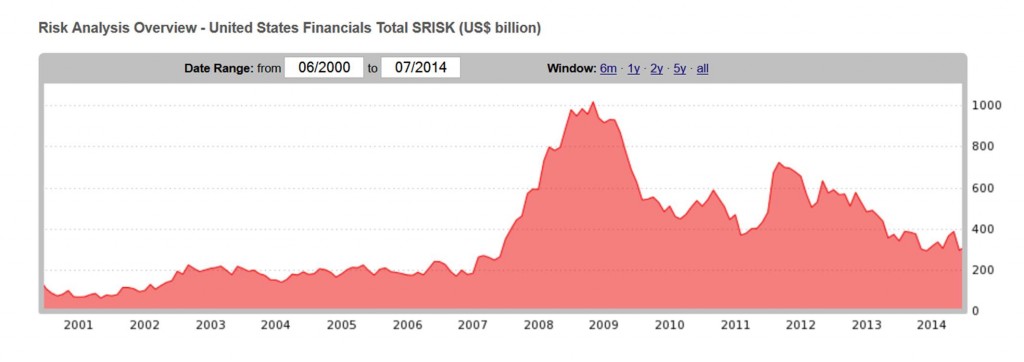

Finally, the same Systemic financial risk graph of America:

Don't let the GOP make you believe that Democrats are the big spenders here! The worse point was under a GOP administration.

Note: A graph are from NYU -- a measure of systemic risk

The above graph is very positive for Europe (not good, but positive) insofar as the total debt volume is down, mainly because core Europe has squeezed the public expenditures (hence the massive unemployment), so the picture is still positive,if you compare to 2008 its great, but rather bad compared to 2007! Anyway there we are, Europe's basket cases are borrowing cheaply (in the short end of the curve), there is no fear of inflation in Europe (deflation is the real risk here -- same as in America where the economies are working substantially below potential). So rolling the short dated debt presents limited risk for investors.

It makes perfect sense when you consider that European investors have few "choice" options available. The market is seen as "very bubbly" and most investors are already very long the market -- usually with solid profits buffer in their positions, and are therefore unwilling to buy more with the risk of increasing their average costs. Especially hard to justify investing in the CAC or DAX in view of the rather high multiples (the same is true for the American markets). Sure a P/E of 14 can be justified but its considered high when corporate profits as a percentage of GDP are standing at historical high (its hard to see how they can go higher... although).

So for institutional investors the bond market in Europe is the one place they can go, and the search for yield pushes them to the outer edge of Europe (where by the way the population has already been wiped into submission). Things in France are just starting and the population isn't going to take it lying down, no sir!

Investors are logical give a set of options they will seek maybe not the best solution, but the least bad one at least.

On a side note, a European friend recently told me that it was disgraceful how North America's pension funds were changing the rules on pension holders (I didn't mention that the move to replace defined pension to defined contribution occurred years ago). But I did point out that at least in North America we had pension assets -- while in Europe they have nothing! Just a promise to pay -- maybe. He actually didn't believe me! (ok not really a friend more of an aircraft acquaintance really) I explained to him that in North America the pension assets belong to the "pensioners" while the promise from European governments (and companies) was just that. In fact, I pointed out that after Enron it became illegal for pension funds to invest in their own company (no more than 5% of assets) to avoid having a bankruptcy killing both your job and your pension. I suggested that he check with his own company...

Finally, China does weird stuff -- this video, says so much about China's risk management culture. The video (from a dashcam) shows the demolition of a building in the middle of a city, people are walking nearby unaware that the building is about to go down. Rather spectacular. It reminds me of a book a read a few years ago: Poorly made in China where a shampoo made in China had on the label: "Not tested on animals" which was absolutely true, since that product had not been tested at all!

Recently, GDP growth in China has been lagging from target numbers -- the solution has been to turn the spigots of money creation full on. The imbalance that the Chinese themselves worry about: Investment Vs, Consumption is worse today than it was 4 years ago. Chinese are used to the way things are and are not ready to assume the very real burden that shifting to a consumption society implies.

hence this:

This is very bad

The NYU measure of systemic financial risk for China this year reached an all-time high. This seems to be a result of the fact that liabilities of the Chinese banks have continued to grow rapidly while stock valuations of the institutions appear quite vulnerable to a downturn. The real issue is one of contagion. When Lehman was "let go" no one thought the repercussions would be so dramatic -- really everyone though there would be some limited contagion, turns out the way our world is connected it doesn't work that way. So imagine a Chinese bank walking away from its derivatives obligation to JP Morgan (or DB for that matter) the largest derivates players? I don't know, my bet is that no else has any idea either!

Finally, the same Systemic financial risk graph of America:

Don't let the GOP make you believe that Democrats are the big spenders here! The worse point was under a GOP administration.

Note: A graph are from NYU -- a measure of systemic risk

Comments